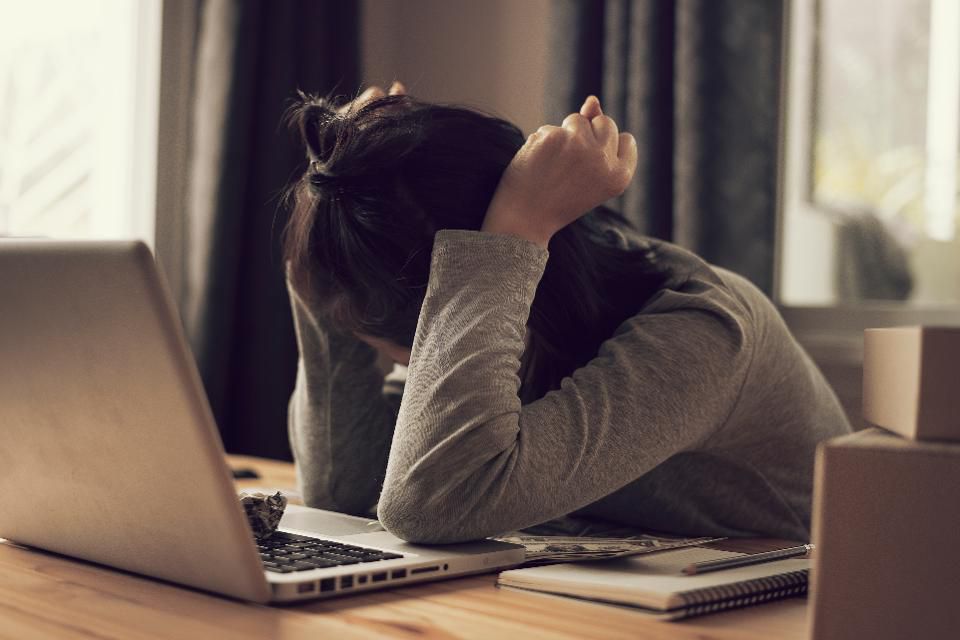

Sometimes employees’ financial stresses get so intense, they become unavoidable management issues. They can reduce productivity and engagement and increase turnover, healthcare utilization, absenteeism and worse. Employers’ resources for addressing this kind of issue are typically very limited.

It’s not unheard of for employees to directly ask their managers for a personal loan to meet an unexpected expense. When personal financial stresses get this, well personal, managers want to be able to address the issues quickly, effectively, appropriately and with existing resources, that is, for free. What’s a manager to do?

First, the manager has to identify that an employee is facing a crisis. This is complicated by the taboo on speaking about money and personal finances. Quintessential American values of self-reliance and personal responsibility make sharing experiences and situations difficult. In my time as a manager, I scrupulously avoided prying into the personal business of my direct reports. So, the most likely way a manager will learn that an employee is financially stressed is only when a crisis so extreme occurs that the employee is motivated to break the taboo and tell the manager directly.

Other clues a manager may not always be aware of include: hardship loans and withdrawals from 401(k) accounts; unusual absenteeism or reduced productivity (e.g., as the employee deals with creditors); underused benefits including HRAs and FSAs and stress-related health issues like backaches, frequent illness, depression, anxiety and sleeplessness.

A common cause for financial distress is the practice of living paycheck-to-paycheck, which affects 49 percent of men and 56 percent of women. Indeed, 63% of Americans don’t have enough savings to cover a $500 emergency. One manager I spoke to told me that two of the four assistants he’s had over his career have asked him directly for a personal loan due to an unexpected expense or a spouse’s loss of employment.

Another frequent cause is excess debt: 70% of Millennials said they consistently carry balances on their credit cards, and 45% use their credit cards for monthly expenses they couldn’t otherwise afford. Finally, there is unexpected or chronic health care costs and older workers who delay retirement due to insufficient savings.

“Many people live with their financial dominoes all aligned and no savings in reserve in case one of them falls” — Byron Haney, AFC.

So what can a manager do that’s free and hopefully helpful?

Depending on the relationship, the manager can offer a sympathetic ear and, if the employee asks for it, offer some common sense ideas and suggestions. Create or find a private space with little risk of distraction or interruption. Use active listening techniques, listening mindfully and without judgment. Be prepared with resources for professional, medical or mental health including the number of the company’s EAP, if any. You may want to check in with the legal and human resources folks to limit any risk to you or your company, even though you are doing the right thing.

Another option is to direct the employee to a non-profit credit counseling agency or perhaps a government agency for assistance. Credit counseling agencies help people manage excessive debt, improve credit scores, manage student loans, undergo bankruptcy and address housing challenges. A good place to start is the National Foundation for Credit Counseling, which accredits agencies to help ensure quality and trustworthiness. Encourage the employee to take the time to shop around for the best fit with questions like these. Some credit unions also offer counseling and advice. Low-income employees may get counseling advice about money matters and public assistance from the local government. For example, New York City’s Office of Financial Empowerment may be a good place to start.

These steps will demonstrate the manager’s concern for the employee and give the employee a constructive next step to handle their crisis. But you’re not done. The taboo on talking about personal finance and the widespread incidence of financial stress in this country means it’s likely that other employees are suffering as well, even if they are not saying anything (yet). A proactive manager will take some steps to identify and attempt to address these stresses before they compound and surface to disrupt the workplace.

Consider what you can do to help build a community in which talking about personal finances, and other personal challenges and opportunities are more normal and even encouraged. For example, personal finance can be included in an existing mentorship program. Nonprofit counseling agencies, credit unions and fee-only financial planners may be willing to lead a discussion and provide some financial education for free.

Personal finance is hard. Employees often lack even basic financial literacy and are surrounded by marketing noise and information of dubious trustworthiness. Many are stressed by the demands of work, family and making ends meet. If your employees are like Americans in general, most of them are financially stressed and at risk of getting behind on their bills. Caring, proactive managers can invest a little time (and no money) and help employees get the immediate help they need while building relationships, trust and productivity. While employers are increasingly investing in more fundamental and likely more effective steps to improve employee financial wellness, a little homework and time can go a long way.

{kind=link}

{kind=link}

{kind=link}

{kind=link}